Why Insurance Claims Get Denied —

Even When You’ve Paid for Years

When Doing Everything “Right” Still Isn’t Enough

Few moments feel as destabilizing as opening a denial letter after years — sometimes decades — of faithfully paying insurance premiums.

You didn’t skip payments.

You didn’t lie on your application.

You didn’t expect special treatment.

You expected the coverage you were promised.

And yet, your insurance claim was denied.

For many policyholders, this moment triggers more than financial stress. It shakes confidence in the system itself. People begin asking:

Did I misunderstand my policy this badly?

Is this even legal?

If insurance doesn’t pay when I need it, what was I paying for all those years?

At ICE, we see this moment every day. And here’s the truth most insurers never say out loud:

Insurance claim denials are rarely about whether you were a “good customer.”

They’re about rules, interpretations, and incentives that operate quietly in the background.

Understanding those forces is how you move from panic to power.

The Core Issue Explained:

Insurance Isn’t a Promise — It’s a Filter

Most people think insurance works like this:

“I pay my premiums. If something bad happens, my insurer helps cover the loss.”

But insurance policies aren’t written as simple promises. They are risk-transfer contracts designed to define, narrow, and control when money leaves the insurer.

“You’re covered for losses under this policy.”

What the policy actually means

Coverage applies only if all of the following are true:

The cause of loss fits a defined category

No exclusions apply (even indirectly)

All policy conditions are met exactly

Deadlines are followed precisely

Documentation meets internal standards

The insurer’s valuation method supports payment

Miss any one of those, and an insurance claim can be denied — regardless of how long you’ve been paying.

Loyalty doesn’t override language.

History doesn’t outweigh definitions.

Premiums don’t guarantee approval.

Claims are evaluated one file at a time, not relationship by relationship.

Most people think insurance works like this:

Why Insurance Claim Denials Are So Common

Insurance denials aren’t anomalies. They’re structural.

The system is designed to create friction at the moment money would otherwise change hands.

Common reasons an insurance claim is denied

Policy Exclusions Hidden in Plain Sight

Exclusions don’t always look dramatic. Many are buried in endorsements, definitions, or cross-references that most policyholders never read — and wouldn’t reasonably understand even if they did.

Ambiguous Language Interpreted Narrowly

When language is unclear, insurers typically interpret it in the way that limits coverage, not expands it.

Missed Deadlines or Technical Violations

Late notice. Incomplete forms. Delayed documentation. These procedural issues are among the most common — and most frustrating — reasons an insurance claim gets denied.

Under-Scoped Damage Assessments

What the adjuster documents often becomes the ceiling of the claim. Damage that isn’t captured early may be excluded later.

Valuation Disputes

Actual Cash Value (ACV) vs. Replacement Cost disputes routinely shrink payouts — sometimes by tens of thousands of dollars.

Recorded Statements Used Against You

Casual comments made early, without guidance, can later be framed as inconsistencies or admissions.

The Incentives Behind the Curtain

To understand why your insurance claim was denied, it helps to understand what insurers are rewarded for.

Insurance companies are financially incentivized to:

This doesn’t require bad actors. It’s built into performance metrics, internal workflows, and cost-control systems.

A well-known consumer advocate once summarized it perfectly:

Insurance works well when nothing goes wrong. Claims expose the fine print.

What a Denial Letter Really Is

Most denial letters feel definitive. Final. Unchallengeable.

They’re not.

A denial letter is best understood as:

The insurer’s opening position — not the last word.

It tells you how they are interpreting the policy right now, based on the information they’ve chosen to consider.

And that means it can change.

what policyholders can do

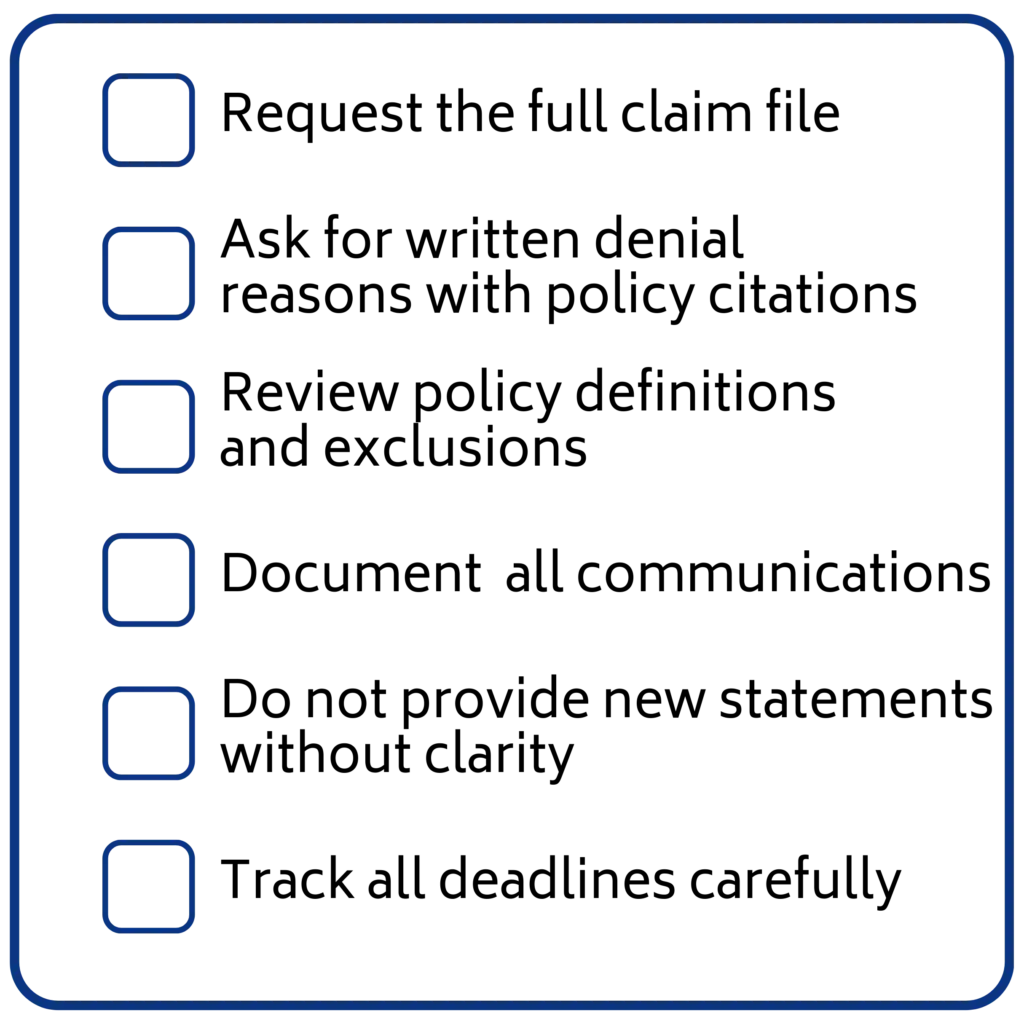

After an Insurance Claim Is Denied

The moment after a denial is where outcomes are decided. Small steps — taken calmly and strategically — often make the difference.

immediate action checklist:

Internal appeal windows

Reinspection requests

Supplemental claim submissions

Regulatory oversight

Small procedural steps often determine whether a denial stands.

key leverage points

Most Policyholders Miss

Even when an insurance claim is denied, several pressure points often remain:

Internal appeal processes

Reinspection requests

Supplemental claim submissions

Policy interpretation challenges

Regulatory oversight and complaints

Insurers rely on the assumption that most people won’t push further. Many denials stand simply because no one challenges them properly.

When to Escalate or Seek Help

Escalation isn’t about being combative. It’s about restoring balance.

You should consider escalation when:

The denial relies on vague or circular explanations

Policy language is selectively quoted

Valuations don’t reflect real-world costs

Communication becomes inconsistent, delayed, or evasive

Escalation options include:

Formal internal appeals

State insurance department complaints

Independent claim reviews

Professional claim advocacy

Accountability is not aggression. It’s participation.

“Most consumers assume a claim denial is final. In reality, many denials are based on incomplete investigations or narrow interpretations that can be challenged.”

— Consumer insurance advocacy perspective, widely echoed by regulatory bodies

The Short Version:

How ICE Helps Level the Playing Field

ICE exists because policyholders are routinely expected to navigate professional-grade systems without professional-grade support.

We help people who’ve had an insurance claim denied by:

Translating policy language into plain English

Identifying weak points in insurer logic

Structuring documentation and responses

Preventing common self-sabotaging mistakes

Creating clarity where confusion is used as leverage

We don’t sell fear.

We don’t promise miracles.

We deliver clarity, strategy, and balance.

The Short Version

Paying premiums doesn’t guarantee approval

Insurance claim denials often rely on technicalities

Policy language matters more than loyalty

Documentation and timing are critical

You usually have options after a denial

You’re not imagining the imbalance

final thoughts:

This Isn’t the End of the Story

If your insurance claim was denied, it doesn’t mean you failed.

It means the system operated exactly as designed — and now you get to respond with information, not emotion.

You’re not alone.

You’re not powerless.

And this is not the end of the story.

⚖️ Educational content only. Not legal or financial advice.